Share Market Update – Schloss Bangalore Share Price Target 2025

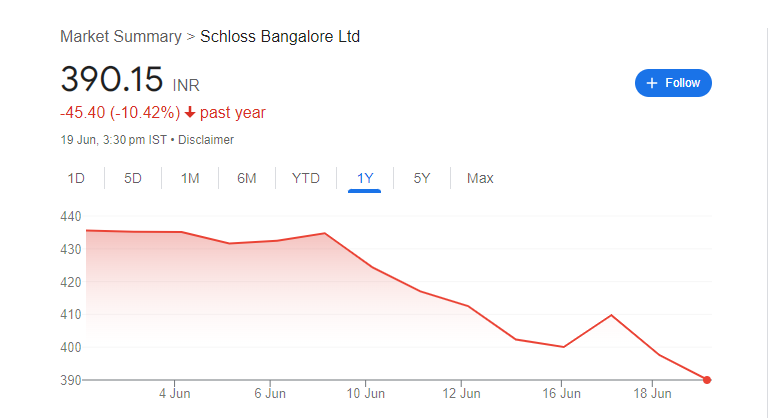

Schloss Bangalore Share Price Target 2025:- Schloss Bangalore Limited is the company that owns and operates the well-known Leela Hotels brand in India. Backed by Brookfield, Schloss manages a collection of luxury hotels across major cities like Delhi, Bengaluru, Mumbai, and Chennai. The company is focused on offering premium hospitality experiences through elegant design, top-tier service, and a strong brand reputation. Recently, Schloss raised funds through an IPO to reduce its debt and support future expansion. Schloss Bangalore Share Price on NSE as of 20 June 2025 is 390.15 INR.

Schloss Bangalore Ltd: Current Market Overview

- Open: 397.65

- High: 398.00

- Low: 382.50

- Mkt cap: 13.03KCr

- P/E ratio: 226.34

- Div yield: N/A

- 52-wk high: 439.90

- 52-wk low: 382.50

Schloss Bangalore Share Price Chart

Schloss Bangalore Share Price Target 2025 (Prediction)

| Schloss Bangalore Share Price Target Years | Schloss Bangalore Share Price Target Months | Share Price Target |

| Schloss Bangalore Share Price Target 2025 | January | – |

| Schloss Bangalore Share Price Target 2025 | February | – |

| Schloss Bangalore Share Price Target 2025 | March | – |

| Schloss Bangalore Share Price Target 2025 | April | – |

| Schloss Bangalore Share Price Target 2025 | May | – |

| Schloss Bangalore Share Price Target 2025 | June | ₹400 |

| Schloss Bangalore Share Price Target 2025 | July | ₹410 |

| Schloss Bangalore Share Price Target 2025 | August | ₹420 |

| Schloss Bangalore Share Price Target 2025 | September | ₹430 |

| Schloss Bangalore Share Price Target 2025 | October | ₹440 |

| Schloss Bangalore Share Price Target 2025 | November | ₹450 |

| Schloss Bangalore Share Price Target 2025 | December | ₹460 |

Schloss Bangalore Shareholding Pattern

- Promoters: 75.91%

- FII: 8.6%

- DII: 7.04%

- Public: 8.45%

Key Factors Affecting Schloss Bangalore Share Price Growth

Here are 5 key factors that could influence Schloss Bangalore (owner of The Leela hotels) share price outlook toward 2025:

1. Occupancy & Revenue Recovery Post-IPO

Schloss reported around 70% average occupancy in FY 2025, trailing its peers (~78–79%). Improvements in room occupancy and revenue-per-available-room (RevPAR) will be critical to justify its premium valuation.

2. Debt Reduction Using IPO Proceeds

The company raised over ₹2,700 crore to repay debt—reducing liabilities by ~32% to ₹25.7 bn. Further debt cuts and interest expense reduction could free up cash flow for expansion or re-investment.

3. Brand Strength & Expansion Pipeline

Backed by Brookfield, Schloss operates 12 existing Leela hotels and plans to add 8 more properties (~833 rooms) by 2028, including key locations like BKC Mumbai, Agra, Srinagar, and Ranthambore.

4. Anchor Investor Support & Institutional Credibility

During the IPO, marquee institutional investors like Goldman Sachs, Fidelity, and Norges Bank came on board, demonstrating confidence in the brand and long-term prospects.

5. Favorable Macro & Luxury Hospitality Tailwinds

India’s luxury hotel segment is forecast to grow significantly (market estimated at ~$31 bn by 2029). As travel rebounds, Schloss stands to benefit—especially if it can maintain leading ESG and service metrics.

Risks and Challenges for Schloss Bangalore Share Price

Here are 5 key risks and challenges that could affect Schloss Bangalore (The Leela hotels) share price target for 2025:

1. High Leverage & Interest Costs

Schloss has a significant debt burden (~₹3,900–4,000 cr) and its interest expense consumed over 30–40% of revenue in FY25. Although debt is being reduced via IPO proceeds, lingering leverage could continue to pressure profitability.

2. Historical Losses & Net Worth Concerns

Despite turning marginally profitable in FY25, the company posted net losses in FY23 (₹62 cr) and FY24 (₹2 cr), and carried negative net worth until 2024. Any recurrence of losses could erode investor confidence.

3. Revenue Concentration in Few Properties

Over 90% of revenue comes from five flagship Leela hotels. Any regional slowdown, property-specific issue, or shift in tourist demand could disproportionately impact financial performance.

4. Aggressive Valuation at Listing

The IPO was priced at ~300× projected FY25 earnings and ~26× EV/EBITDA—well above peer multiples. The weak 7% listing discount suggests that the market sees valuation risk if growth or margin momentum falters.

5. Sector Volatility & Execution Risk

Luxury hospitality is sensitive to economic cycles, seasonal demand, geopolitical tensions, or health crises. Additionally, ongoing debt repayment, hotel renovations, and planned expansion depend on flawless execution; any misstep could pressure occupancy and RevPAR.

Read Also:- Share Market Update – Beezaasan Explotech Share Price Target 2025